© 2017 All Rights Reserved. Do not distribute or repurpose this work without written permission from the copyright holder(s).

Printed from https://www.damninteresting.com/death-by-derivatives/

In April of 1873, an unhappy man walked along Clark Street in downtown Chicago. His name was Aymar de Belloy. There was a gun in his pocket, and a nickel – enough for one final glass of beer.

He entered Kirchoff’s tavern and sat at a table, then changed his mind about the beer. He drew his gun, pointed it at his forehead, and pulled the trigger.

The bullet careened along the inside of his skull like a speed skater on a banked turn. It stopped at the left temple, sparing his brain. Belloy rose and staggered to the bar, shaking hands with the horrified men he passed along the way. Upon reaching the bartender, he apologized in all sincerity for the inconvenience he had just caused. Then he collapsed.

Belloy was a speculator, or “plunger” as they were then known, at the Chicago Board of Trade, where traders negotiated contracts for the future sale of wheat and other such goods. The value of these contracts was based on, or derived from, the current price of wheat. Hence they would one day take the name we use today: derivatives.

In the 1870s, with few rules in place, a man could make a fortune plunging wheat. He could also lose a fortune, and with it the will to live. Indeed, the string of early derivative traders taking their own lives grew long enough that one writer gave it a name: the “crimson thread of suicide.”

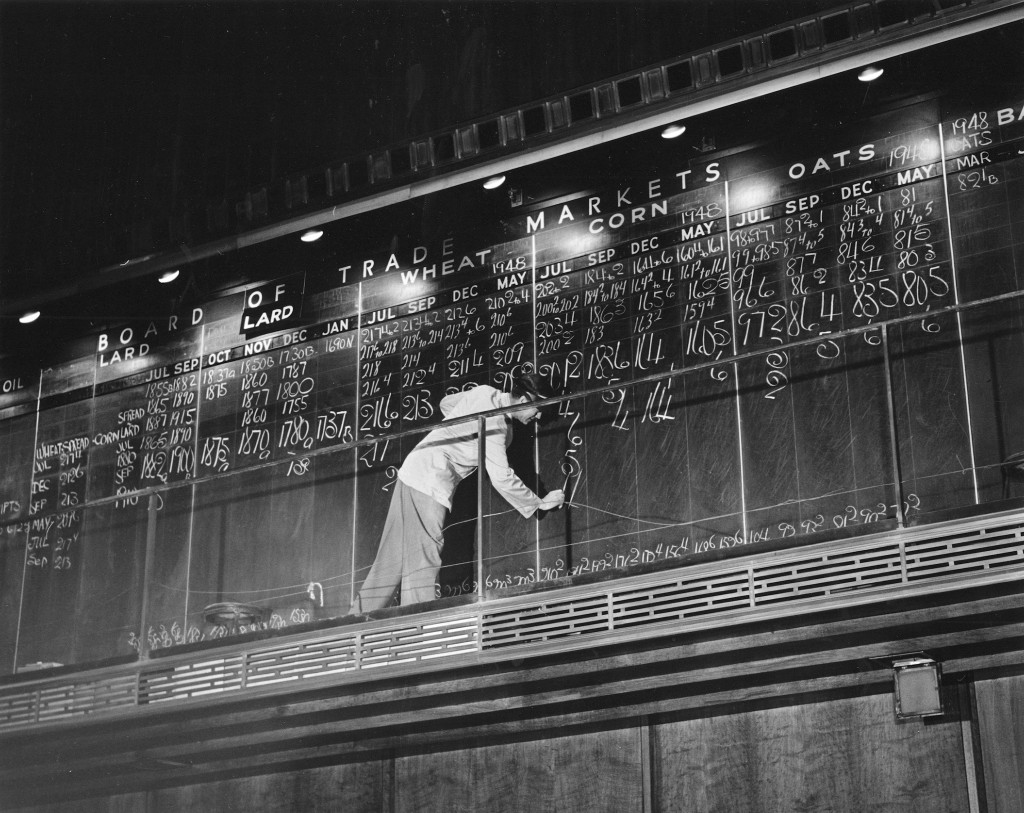

The scale of today’s derivatives market is almost too vast to comprehend. It’s measured in trillions of dollars. Traders, aided by the most sophisticated software money can buy, place bets — billions per second — on the future prices of every manner of stuff. The market hardly exists in any tangible physical sense; most trading takes place across a network of countless devices at data centers around the world.

But in 1873, the global derivatives market was centered in one building on LaSalle Street in Chicago. And it would not have existed at all were it not for the digging of a very long ditch some 25 years earlier.

In 1848, an army of Irish immigrants finished digging the Illinois and Michigan Canal. It was ninety-six miles long and surprisingly shallow—a tall man could stand on the bottom and not dampen his bowler. The canal connected the Chicago River with the Illinois River, which in turn fed the mighty Mississippi, opening an inland waterway from New Orleans to New York. 1848 was also the year Chicago saw its first railway, and stockyard. Its first telegraph and steam-powered grain elevator? Same year.

Indeed, a city’s annus mirabilis (“wonderful year”) doesn’t get much more mirabilis than Chicago’s 1848. These advances would soon turn the city into, well, Chicago, simply by making it so much easier for stuff to move between east and west.

And boy oh boy did stuff thus move: grain, lumber, salt, sugar, pigs, and cattle began floating or rolling into this town on the southern tip of Lake Michigan like never before. There it was unloaded, weighed, graded, sold, stored, and reloaded onto boats or trains heading the other way.

")

In March of 1848, a dozen or so businessmen gathered to form an alliance of business interests, or what we would today call a trade association. It was a brilliant idea whose only problem was the apparent lack of anything for these fellows to actually do. Founders of the Chicago Board of Trade were determined to find something, but interest soon began to wane. To persuade members to show up for meetings, the founders began offering a free lunch of crackers, cheese and ale. Lines soon formed at the door, filled with men from all walks of life who were only too happy to attend meetings in exchange for free booze—or what we would today call, well, a trade association. The Chicago Board of Trade hired a bouncer to keep the freeloaders at bay, but this still left the nascent organization with very little to do. That would soon change.

Before 1848, farmers carted sacks of wheat into the city, behind horses on unpaved roads, and then sold it directly to buyers. When the canal and railroads lowered shipping costs, far more of the golden grain poured into the city, where it was loaded into grain elevators in exchange for a receipt.

With wheat no longer associated with an individual farmer, it became an exchangeable common good, or commodity, with one bushel of a given grade as good as any other. This at last gave the Chicago Board of Trade something to do: It provided an exchange, a place where buyers and sellers could gather in pits and shout out prices at which they were willing to trade.

It didn’t take long for traders to innovate in this new space. In addition to trading wheat already in an elevator, known as physical wheat, they made deals for so-called future wheat not yet in an elevator but expected to arrive at some later date. Such “to-arrive” contracts would eventually take the name used today: futures. Anyone planning to buy or sell future wheat could lock in a price days, weeks, or months in advance. This, of course, required someone to be on the other side of the trade. Sometimes a miller could find a farmer willing to sell, or vice versa, but not always. Enter the plungers.

These fellows had no interest in actually buying or selling grain. They wanted only to profit on price changes, caring not a whit about wheat. They would buy an elevator receipt simply on a hunch that prices would rise, at which time they could sell it at a profit. Or, if the trader foresaw a price decline, he could borrow someone’s receipt, sell it for cash, and later buy it back at a lower price in order to return it to its lender, keeping the difference as a profit. (This is known as shorting a market and is precisely how short selling of stock works today.)

One such plunger was Aymar de Belloy. A French nobleman, scion of one of the oldest and most prominent families in France, Belloy started adulthood with an inheritance of $300,000 ($9 million in today’s dollars)—most of which he immediately proceeded to squander. In 1868, he brought the remnants of his fortune to Chicago to speculate on wheat. He managed to stay afloat long enough to marry and father a number of children, then his luck ran out. And so did the last of his money.

Belloy’s misfortune stemmed from more than bad luck. He was the victim of unscrupulous traders known simply as operators, who might sell fake elevator receipts, or move prices in their favor by spreading false news. Or they might pull off an especially cunning manipulation known as a corner, in which they would buy future wheat while simultaneously buying all physical wheat.

Later, when it came time for the operator to take delivery of his future wheat, the other trader had to first go buy some. But there was none. The operator owned it all. Thus trapped, or cornered, the victim had no choice but to pay whatever price the operator demanded. Cornering was the ruin of many a trader, like our Belloy, to whom the only apparent recourse was to find the nearest saloon and shoot himself in the head.

After an agonizing ride home in a horse-drawn taxi, Belloy’s luck turned in his favor. A doctor pronounced the wound non-life-threatening, assuring Belloy he would be back on his feet in only a week or two. His friends at the Board of Trade took up a collection and raised more than $1,000 for Belloy and his family. Members of the press, having little respect for men who gambled on the price of food, were not so moved. The Chicago Journal ran an editorial on Belloy and his roller-coaster luck. They, too, suggested a collection be taken: to buy him a better gun.

But Belloy’s luck changed again. The doctor was wrong. The wound proved mortal. Two days after shooting himself at Kirchoff’s, the nobleman-turned-derivative-trader died.

The failed plunger left his widow and children penniless. The eldest son went to work as a bootblack on the streets of Chicago, shining shoes, though he himself wore none. Then the boy sold newspapers and scrounged the odd penny however he could. The mother took alms.

The corner practice did more than add to Chicago’s widow and orphan population. It made a mockery of a free market. Farmers might not mind when the price of grain was manipulated upward. They could make more money. But consumers certainly minded. Bakers had to make loaves of bread smaller to keep them priced at a nickel, the most it was believed consumers would pay.

The Board of Trade directors knew something had to be done, so they introduced a new rule:

“…the practice of “corners,” of making contracts for the purchase of a commodity, and then taking measures to render it impossible for the seller to fill his contract, for the purpose of extorting money from him, has been too long tolerated… these transactions are essentially improper and fraudulent.”

The rule could not have been more clear in defining a corner and its ill effects. It went on to proscribe strict penalties for violation and was written into bylaws with haste. And then it was promptly ignored.

On 28 April 1885, members of the Board of Trade and their wives looked forward to a magnificent banquet to be held that evening in the lobby of their gleaming new building at LaSalle Street and Jackson Boulevard. Nearby, the anarchist Albert R. Parsons raised enthusiasm of another sort, telling a gathering crowd on Market Street that the nearly $2 million spent on the building had been stolen from their own pockets, by members of what he dubbed the Chicago Board of Thieves. He called his audience to arms. “Let every man lay up a part of his wages,” he urged them, “buy a Colt’s navy revolver, a Winchester rifle, and learn to make and use dynamite!”

The mob did as instructed. As day turned to dusk, some 2,000 protesters marched toward the building carrying red and black flags, revolvers, and homemade nitroglycerin bombs. A marching band played the Marseillaise. Just one block away from the brightly lit building, a wall of police officers stopped their advance. Mob leaders shook their fists, yelled more words of outrage to the crowd, then retreated to nearby saloons to safely drink off their rage.

The imposing new Board of Trade building may have looked staid and dignified on the outside, but the view inside was anything but. A popular saying went: “The wheat pit is only twenty yards across, but it goes down to hell.” The writer Frank Norris penned a roman-a-clef titled The Pit about wheat speculation in Chicago. It was not a dry read. He described the trading pit, for instance, as:

“a great whirlpool, a pit of roaring waters spun and thundered, sucking in the life tides of the city, sucking them in as into the mouth of some tremendous cloaca, then vomiting them forth again, spewing them up and out, only to catch them in the return eddy and suck them in afresh.”

The image becomes particularly disturbing upon learning the definition of the word “cloaca”.

The unlucky Belloy was not the only early futures trader whose life ended in an unpleasant fashion. The ruined trader Nelson Van Kirk used his last few dollars to buy a cheap revolver that had to be pried from the fingers of his corpse. The trader T.C. Chisolm lost everything in a failed wheat corner, save an elevator full of corn in New York, which, it turned out, was rotten. He took a ferry to Brooklyn (no doubt noticing a magnificent new bridge still under construction), then found a remote slip where he filled his pockets with stones and plunged into the East River to drown.

Deaths such as these became rather routine. In 1905, the veteran CBOT official George F. Stone was asked about the long history of out-of-luck traders resorting to felo de se. He rejected the idea that board members were prone to suicide, and in fact asserted just the opposite:

“The average board of trade man is of other mettle. He is hopeful and looks upon the bright side of things, and in case of disaster his first impulse is to consider that better times will come.”

The Belloy, Chisholm, and Van Kirk widows may have begged to disagree.

The manipulation of securities trading continues to this day, such as by high frequency traders whose practices are seen by some as less than ethical. Michael Lewis details one such practice in his book Flash Boys, where market makers use superior networking technology to change the market price of a security after a customer sees it and places an order, forcing them to trade at an inferior price.

The derivative traders once known as operators remain at work, but trader suicide began, thankfully, to wane in the early years of the twentieth century. Plenty of traders have lost fortunes and many died penniless, but typically not at their own hands. Thus we are unlikely to again see the likes of Aymar de Belloy, whose story does not end with his death.

One month after his funeral, Belloy’s luck turned yet again. News came from France that he had inherited $2 million ($50 million today) following the death of his mother. All that was needed for the widow to receive the money was proof of marriage. This was duly secured and provided to the authorities.

Belloy’s widow took the title of Marchioness, the eldest son the title of Marquis. The family was elevated from dire poverty in Chicago’s tenement district to aristocracy on the Gold Coast.

Life after that was pretty good.

© 2017 All Rights Reserved. Do not distribute or repurpose this work without written permission from the copyright holder(s).

Printed from https://www.damninteresting.com/death-by-derivatives/

Since you enjoyed our work enough to print it out, and read it clear to the end, would you consider donating a few dollars at https://www.damninteresting.com/donate ?

First! This is really impressive delivery on top of the story. Love the music insert and the smooth pictures.

P.S. Cloaca. Clackackackackackackacka.

Second!

Third!

Is there a point to this story? People trade and speculate in commodities, and sometimes someone goes bust and pays the price. What are we supposed to learn from this? Hoe is this damn interesting?

Mr. Durbin:

Fantastic article! I’m the compliance officer for a small community bank, and I was unaware of the history of derivatives.

For me, derivatives are proof that the megabanks need to be regulated extremely strongly and watched even more strongly.

They are not to be trusted, and they can do and have done much harm to the middle classes of many countries.

This may be mostly true. And it’s true that cases of market manipulation continue to this day. As do cases of plagiarism and journalistic fraud by reporters; as do cases of malpractice by doctors; as do cases of venality by politicians; as do cases of… well, it turns out humans haven’t changed a whole lot, and unethical practices haven’t died out. Wherever you look.

True story. More on Aymar Ludovic Marshal de Belloy De Saint Lienard at

https://www.ancestry.com/family-tree/person/tree/60243152/person/34053896050/facts

Marla Rothery (de Belloy) Wosnak

Sir, very nice article, would like to read more of yours.

Sir, very nice and informative article, would like to read more of yours, just please use a bit more easily understandable vernacular.

Very interesting and impressive! I like the narrative style and sound effects. If I close my eyes I think I could imagine the scenes as I am watching a movie.